Waymo will begin offering fully driverless robotaxi rides in four new U.S. cities—San Diego, Las Vegas, Tampa, and Denver—starting with employee pilots before a broader public rollout, expanding its lead in the U.S. autonomous-vehicle market; the company plans London service later this year and had about 4,000 robotaxis in its fleet as of May.

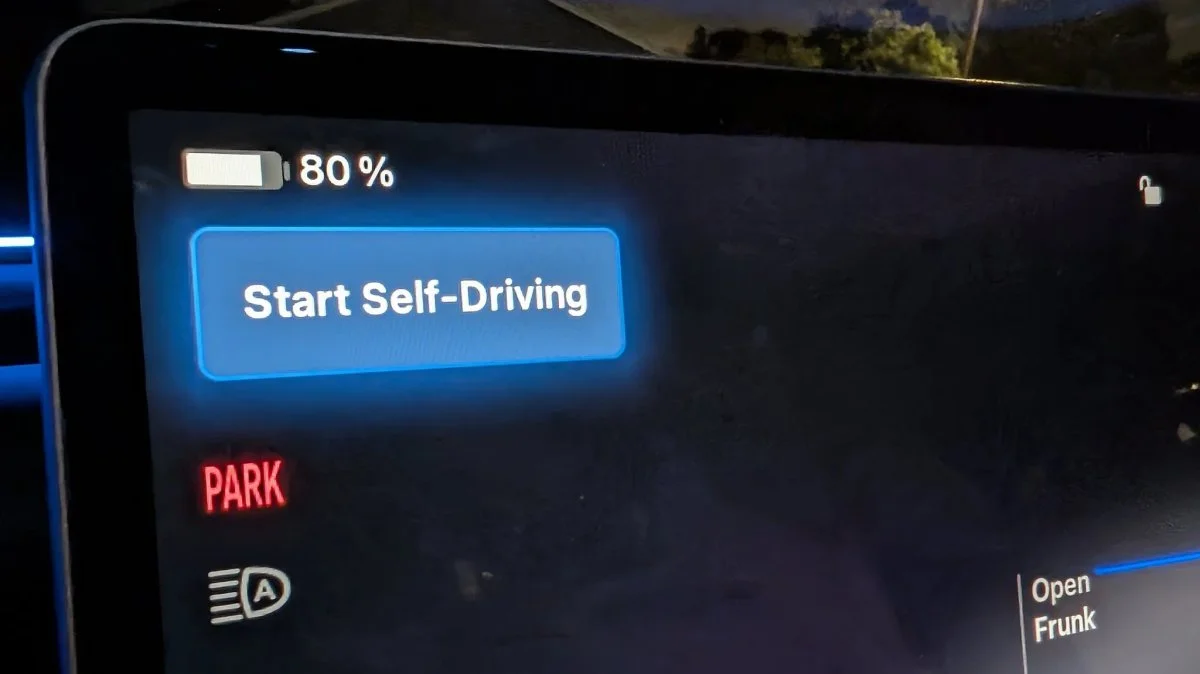

Tesla is releasing FSD v14 Lite to HW3/AI3 cars, a compact version of the newer HW4-based v14 that distills input from AI4 into HW3. It adds features like starting FSD from Park, automatic Reverse/Drive transitions, Arrival Options, and always-on Speed Profiles, plus improved responsiveness, lane-centering, and smoother behavior—though some v14 features (Smart Summon upgrades, the standalone Self-Driving app, and dynamic parking-pin adjustments) are omitted due to hardware limits. The rollout began with early-access testers on software 2026.20.5.1, with broader rollout after validation. Tesla notes HW3 cannot reach unsupervised autonomy and a hardware upgrade path to HW4+/AI5 is planned later; v15 Lite is unlikely. International rollout will follow validation, potentially in EU, Australia, NZ, and Korea in coming weeks.

Tesla has begun rolling out FSD v14 Lite to Hardware 3 cars (AI3), a supervised Level 2 update that distills HW4’s v14 guidance into the HW3 stack to improve city navigation, safety, and added parking/reversing features. The rollout starts with early-access drivers, with a wider release expected in the coming weeks; unsupervised autonomy remains unavailable on HW3, and the update does not fulfill the original promise of full self-driving.

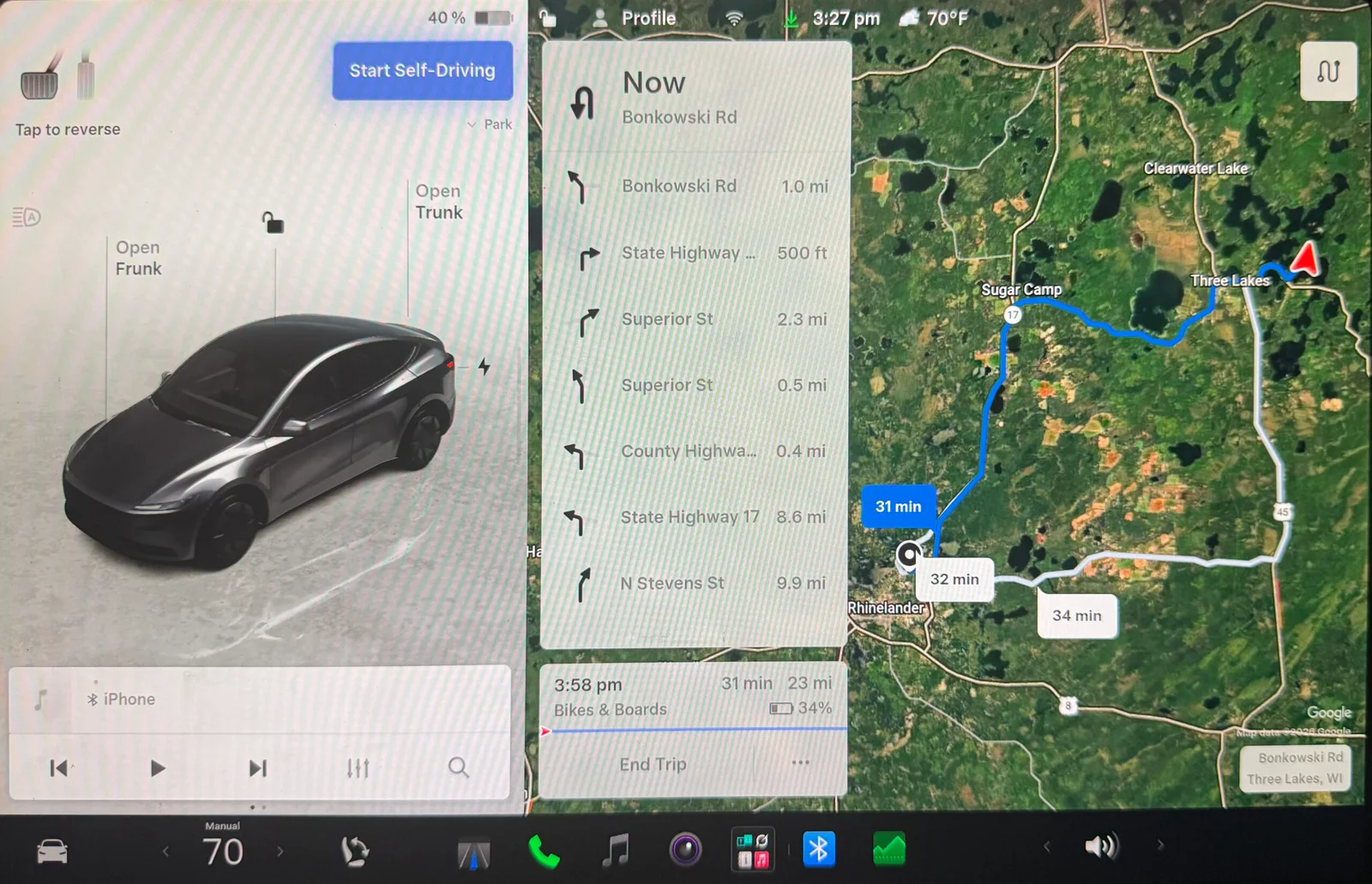

Over two weeks with HW4 and FSD V14 in a 2026 Model Y, the author reports major progress: FSD V14 can start trips, back out of driveways, and navigate with modes from Sloth to Mad Max, effectively acting as a chauffeur while requiring supervision. GPS/map accuracy remains a bottleneck (about 15 feet) with occasional misdirections and parking challenges, especially in garages or lots. The system relies on visible-light cameras (no radar), won’t handle severe weather well, and steering assist requires a $99/month subscription. There are several features still on the wishlist. Overall, notable improvement, but not fully hands-off autonomy yet.

Waymo has begun offering limited free rides in its new Ojai robotaxi—the first purpose-built Waymo vehicle—with the 6th-generation Driver across San Francisco, Los Angeles, and Phoenix. The Ojai emphasizes rider experience and accessibility, features a spacious rear cabin and easier entry, and uses a redesigned hardware stack that cuts sensors by about 42% while increasing capability, enabling snow operation and lowering unit costs to under $20,000. Waymo has now surpassed 20 million autonomous trips in 11 cities and plans broader geographic and production expansion from its Arizona factory to tens of thousands of units per year, while continuing to scale to additional markets beyond the initial three.

Chinese automakers, led by Huawei-backed Maextro with its S800, are pushing into the luxury EV space by offering advanced software, autonomy, and lower prices to take on Rolls‑Royce, Mercedes‑Maybach and BMW, signaling a rising upmarket challenge to European ultra-luxury brands.

Beijing Auto Show 2026 set a record for size and premieres, signaling a shift in which China leads electrification and AI-enabled driving across price tiers. The show showcased high-tech features like lidar, drive-by-wire, and AI chips across affordable and flagship models—from XPeng’s Level 4-focused GX and Li Auto’s L9 Livis, to Geely’s robotaxi EVA Cab and a wave of affordable lidar-equipped EVs. Global automakers partner with Chinese suppliers (Huawei, ByteDance, Momenta, Qualcomm), VW rolls out a range-extended ID. Era 9X, and even a flying-car “land carrier” by Aridge. With Xiaomi’s Vision Gran Turismo concept and other bold concepts, the event underscores China’s rising dominance in EV tech, AI, and new mobility formats rather than a cheap-versus-premium divide.

Elon Musk acknowledged that Tesla’s Hardware 3 cannot deliver unsupervised Full Self-Driving, contradicting years of promises; the company is shifting to Hardware 4 and possible retrofits, but execution timelines, costs, and ongoing legal actions are weighing on investors and raising questions about autonomy timelines and the stock.

Tesla’s upcoming Q1 report is expected to show about $22.2 billion in revenue with earnings around 37 cents a share, but investors are focusing on the company’s long‑term bets—robotaxi expansion, humanoid robots, and potential SpaceX ties—over the near‑term results, amid questions about scaling, regulatory hurdles, and the pace of rollout in new cities.

Tesla’s robotaxi service began in Dallas, but a rider’s experience exposed ongoing reliability and safety concerns: after a long app wait, the vehicle navigated city streets, missed an exit, and briefly pulled onto an 80–90 mph highway before a human operator took over and steered it off. The 11-mile, 54-minute ride wandered to the wrong location and a hotel loop before being redirected, costing about $18. The incident illustrates the promise of autonomous ride-hailing alongside persistent glitches and skepticism about readiness for everyday use.

Uber has expanded a broad slate of robotaxi partnerships with Zoox, Wayve-Nissan, Rivian and others to keep the market open and competitive by avoiding a single dominant supplier. Positioned as the demand aggregator, Uber aims to attract investment into a diversified ecosystem rather than chase one winner. While this could expand the overall ride-hailing market and give Uber more negotiating leverage, most partners have yet to deploy fully driverless paid services and cost/scale remain the main challenges.

Hyundai Motor Group (Hyundai and Kia) expands its partnership with NVIDIA to accelerate data-driven autonomous driving using the DRIVE Hyperion platform, enabling Level 2+ deployment in select vehicles and Level 4 robotaxi development via Motional, by uniting SDV capabilities, large fleet data, and NVIDIA's AI/accelerated computing across production vehicles with ongoing data collection, training, simulation and deployment.

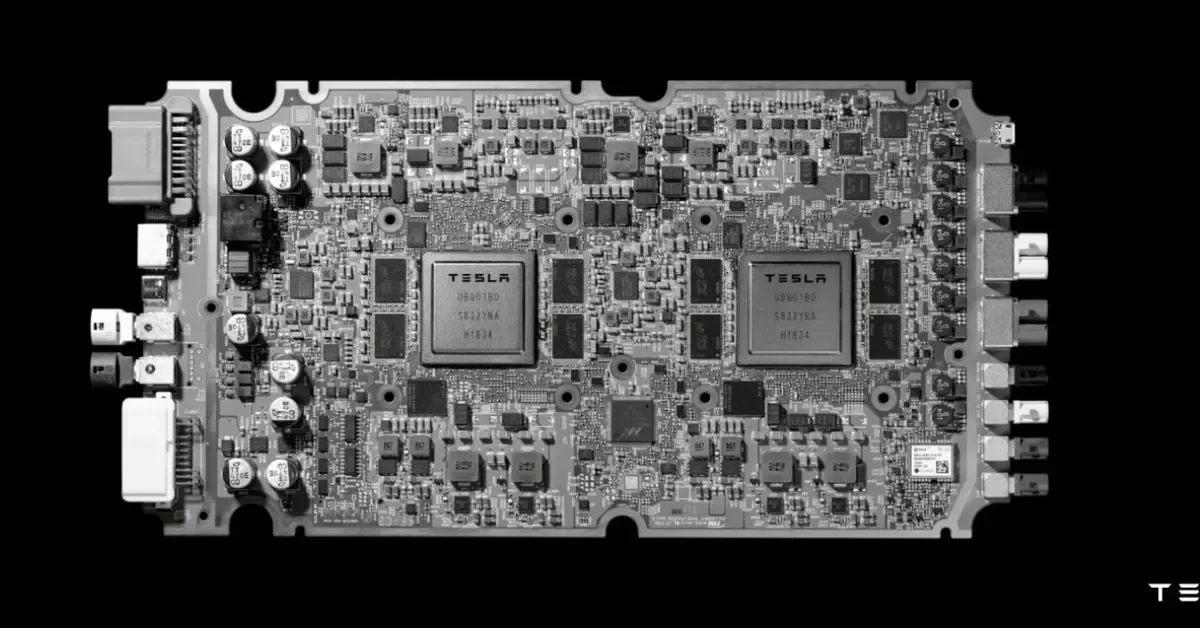

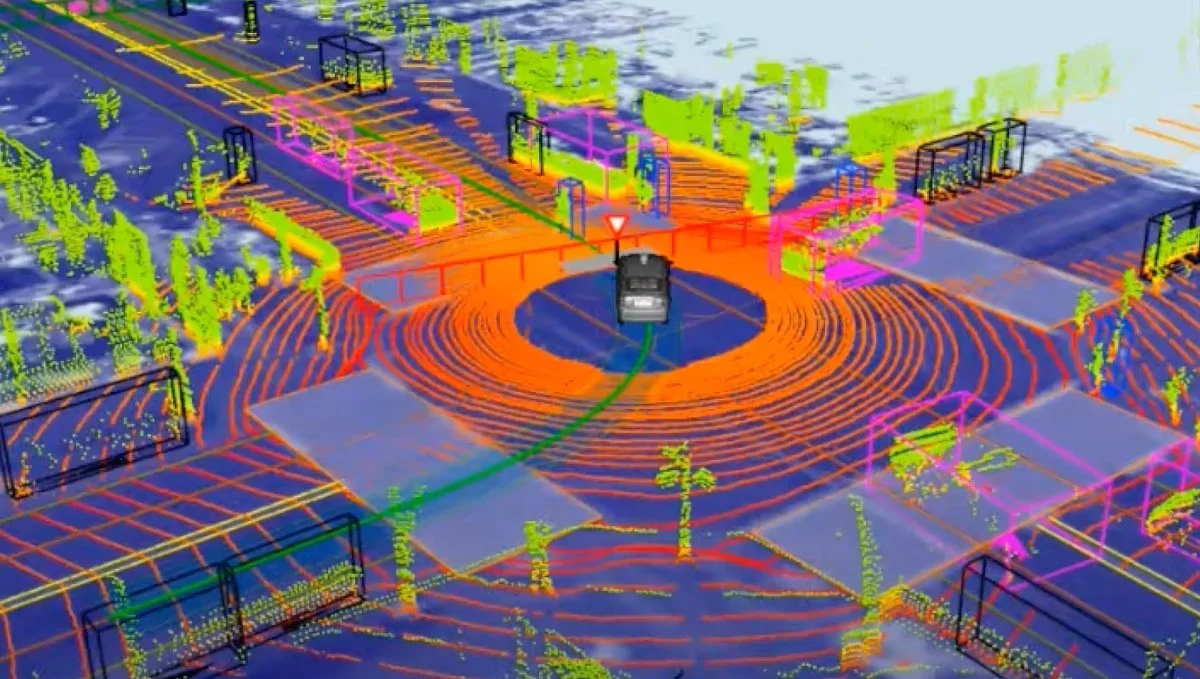

Tesla has doubled down on a vision-only approach, removing radar and relying on eight cameras and a neural-network world model to drive autonomy. The company argues sensor fusion with radar/LiDAR creates conflicting data that can undermine safety, a stance it has pursued since 2021, with radar still present on some cars but not used for FSD. Tesla trains depth and velocity from vast camera data using ground-truth measurements from auxiliary sensors, and uses a foveated processing approach to keep compute scalable by focusing high-res on distant “priority” regions while downsampling the rest. The gamble aims for cheaper, scalable autonomy, contrasting with rivals’ sensor-fusion stacks.

Geely, which controls Volvo, plans to build cars in the U.S. via Volvo’s South Carolina plant, but a new Commerce Department rule requires that all software and connectivity tech be free of Chinese control. Software for model years 2027+ must be certified, with per-model/year authorizations, and hardware bans begin for 2030; no waivers have been issued yet. Volvo may help navigate approvals, but Geely would need to prove software origin and data governance for every model/year before selling in America.

Uber is set to report Q4 and full-year results, with analysts expecting EPS of $0.79 on $14.32 billion in revenue. Beyond the headline numbers, Uber is advancing autonomous-driving pilots with partners like Nvidia, expanding Uber Eats partnerships with Kroger and Loblaw, and possibly exploring mobility-related acquisitions. Options traders anticipate about a 7% post-earnings move, while analysts maintain a Strong Buy with an average target of $112.40 for roughly 44% upside.