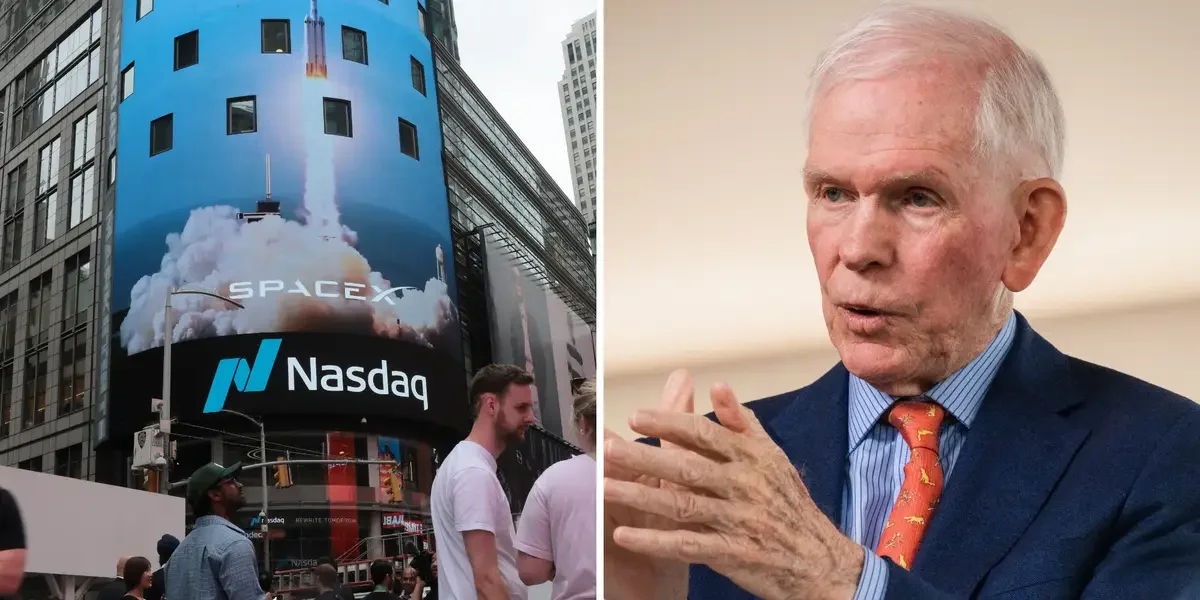

RayJay’s SpaceX bet hints at a $10 trillion future via orbital infrastructure

Raymond James launches SpaceX coverage with a Strong Buy and an $800 target, implying a market cap north of $10tn based on forecasts of about $837B in revenue and $696B in EBITDA by 2031. The bull case hinges on Starship cutting orbital transport costs by over 99% and enabling a broader SpaceX infrastructure play—from connectivity and AI to manufacturing and energy—with Starlink feeding the cycle. The article notes SpaceX’s current ~$18.7B revenue and a ~$4.9B loss last year, while Alphaville’s own satire hints at even more optimistic targets as analysts debate the company’s multi-decade growth potential.