AI memory boom keeps Micron in focus as demand spikes

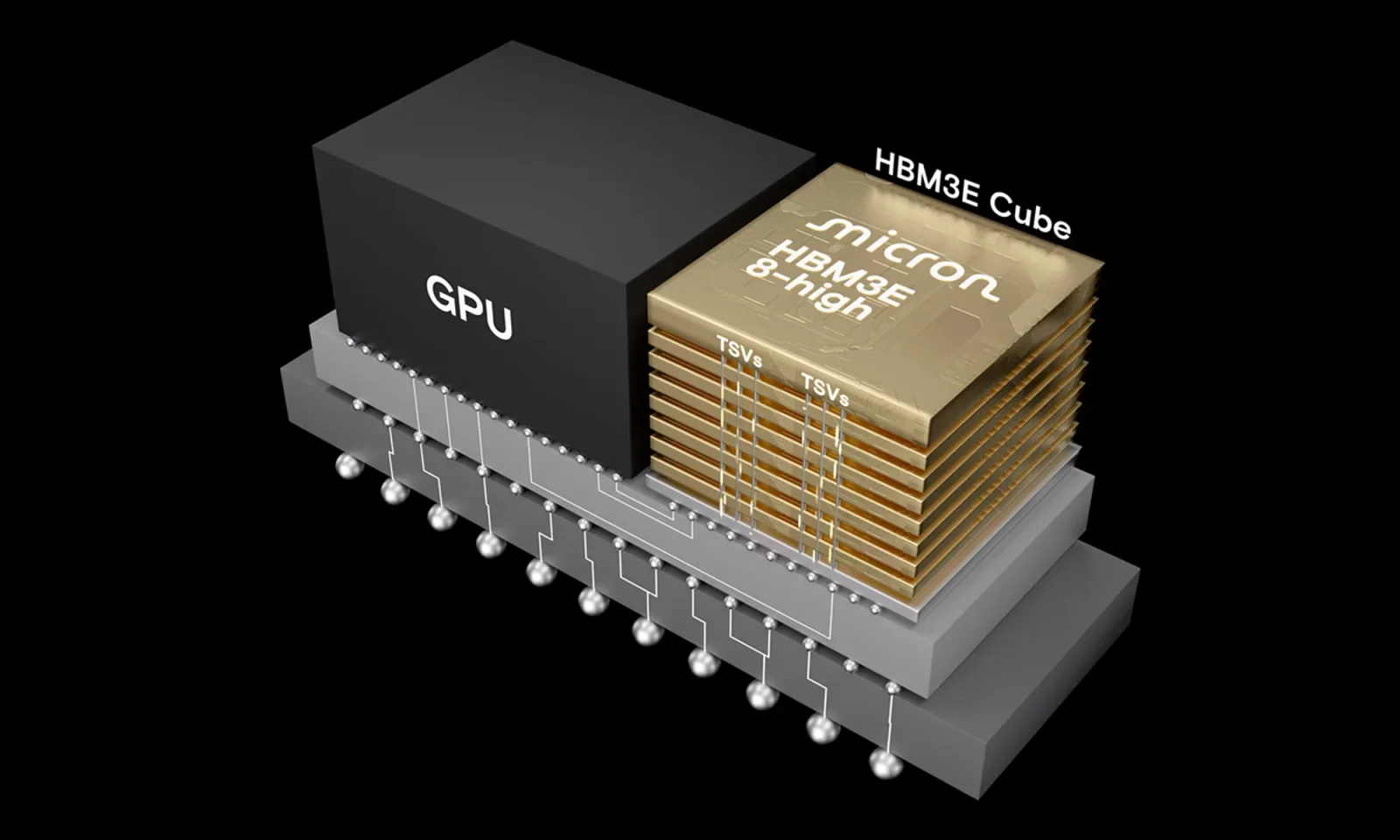

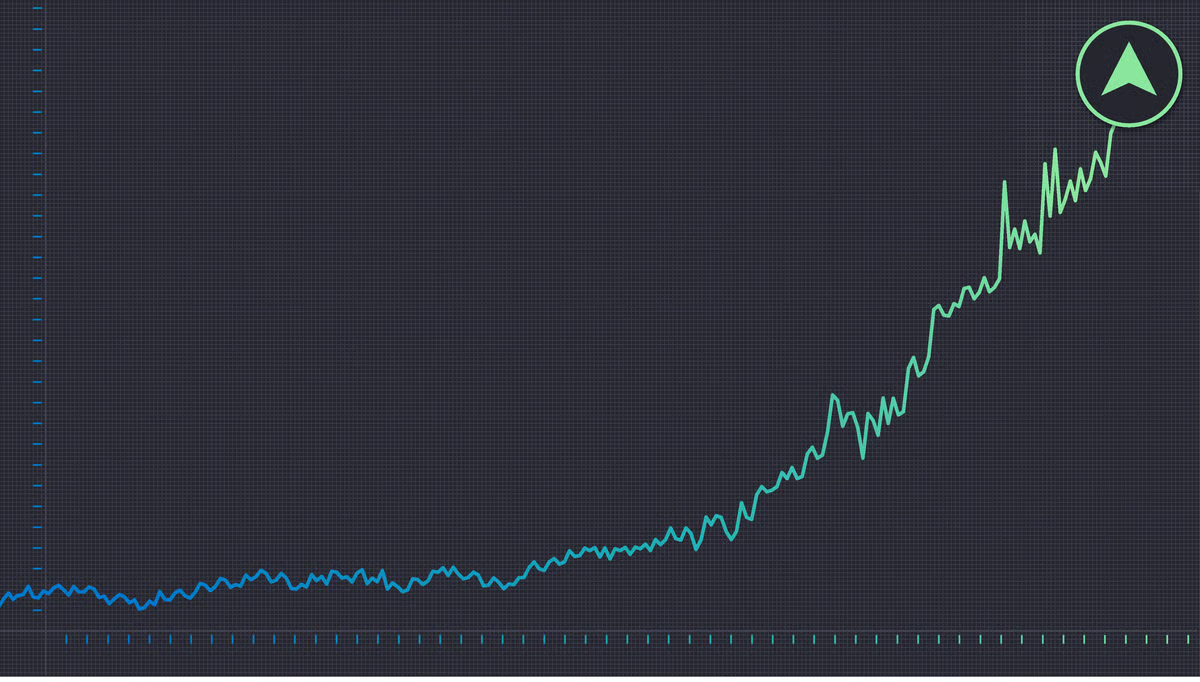

Micron Technology rides a surge in AI-driven memory demand, reporting strong quarterly results and guiding toward about $50 billion in revenue next quarter. Demand spans high-bandwidth memory, DRAM, and NAND, with HBM demand expected to remain tight into 2027–28 as customers lock in capacity. Analysts remain broadly bullish (roughly 29 Buy ratings of 30). The key question for investors is whether Micron can sustain earnings growth to justify its rally, since the memory shortage duration will influence future upside.