A breadth study shows only about 60% of S&P 500 components are trading above their 200-day moving average, signaling a narrowing market leadership and greater fragility as a small group of mega-cap stocks drive gains while the broader index remains vulnerable if leadership wanes.

The S&P 500 surged above 7,000 in a fast rebound led by financials, signaling strong near-term momentum even as breadth remained narrow and the Magnificent Seven lagged; earnings results and broader participation will determine whether the rally can continue, with banks beating expectations and earnings season beginning serving as the next test.

Morgan Stanley’s Michael Wilson argues the S&P 500 is nearing the end of its rolling correction, with earnings growth set to reaccelerate and market breadth improving. However, the pace of oil and dollar moves could keep volatility elevated in the near term and influence how quickly the market flexes out of the correction, potentially creating opportunities in cyclical names.

Investors are rotating away from Big Tech into a broader leadership group, expanding market breadth and helping the S&P 500 push higher in 2026 even as concerns about Fed independence linger. The shift has seen consumer staples rally and smaller/mid-cap stocks gain traction, signaling a more durable, breadth-driven rally beyond the magnified Tech-led moves.

Tech stocks, especially the 'Magnificent Seven,' are driving a record-setting rally on Wall Street, with broad participation indicated by the NYSE A/D line, though concerns remain due to a lower percentage of stocks trading above their 200-day moving averages. The rally is supported by positive economic outlooks, trade developments, and potential Fed rate cuts, but its sustainability depends on continued sector-wide strength.

The U.S. stock market is experiencing a rare and concerning phenomenon known as 'bad breadth,' where more stocks are falling than rising despite the S&P 500's continued climb. This situation, not seen in over 20 years, is reminiscent of the period around September 11, 2001. While megacap technology stocks are currently offsetting broader market weakness, the narrow market breadth is causing investor anxiety. Historically, such weak breadth has coincided with significant market downturns, raising concerns about potential future declines.

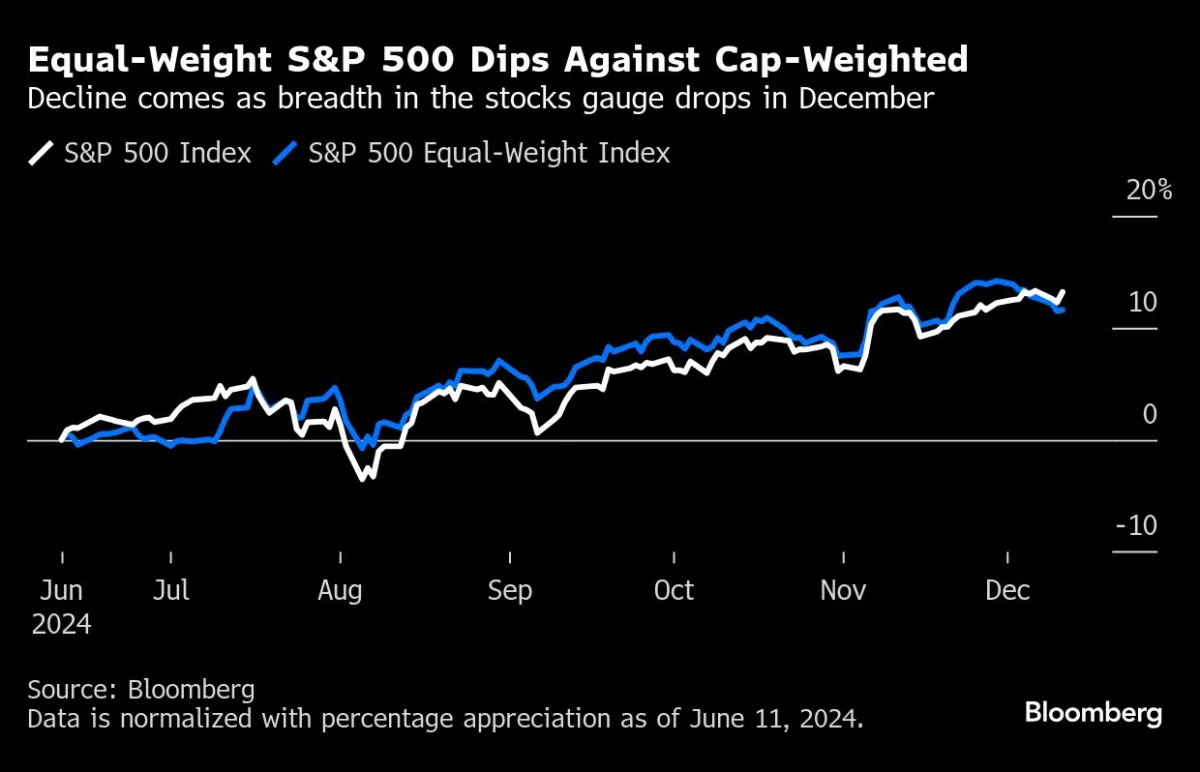

The S&P 500's recent rally is showing signs of weakness as fewer stocks are contributing to its gains, with technology giants like Alphabet and Microsoft driving the index higher while many other stocks decline. This trend, known as poor market breadth, suggests a fragile foundation for the rally, raising concerns among strategists about stretched valuations and elevated positioning. The equal-weight version of the S&P 500 has been declining, indicating that the rally is not broad-based, and some analysts warn of a potential sell signal if the trend continues.

The U.S. stock market's "bad breadth" is causing concern among some bullish analysts as only a few megacap tech stocks continue to drive the main indexes higher, with the "Fantastic Four" (Microsoft, Nvidia, Meta Platforms, and Amazon) contributing roughly 70% of the S&P 500's year-to-date gains. Market breadth deterioration and stretched market sentiment are signaling a potential near-term peak for stocks, with some analysts warning of a possible pullback in the coming weeks. Despite finishing at record highs, U.S. stocks opened the new week in the red, with the S&P 500 down 0.5% and the Dow Jones Industrial Average down 0.9% amid concerns about the timing of interest rate cuts.

The 2023 stock market rally has entered a healthier phase, with sectors like financials and small caps surging. Research shows that 78% of S&P 500 stocks were above their 200-day moving average last week, indicating broad market strength. The rally is no longer solely driven by the Magnificent 7 tech stocks, as other stocks in the S&P 500 have joined the front. Stocks like Bath & Body Works, Illumina, and Norwegian Cruise Lines have outperformed the Magnificent 7 in the past month. The market rally has also broadened out to include sectors like Financials, Industrials, and Real Estate. If this trend continues, it could indicate a healthier and more sustainable bull market for 2023.

The recent losses in the S&P 500 could be healthy for the overall index, according to some Wall Street strategists. The dominance of the "Magnificent Seven" stocks, which have driven much of the index's gains this year, has led to concerns about market breadth. Market breadth refers to gains being distributed across companies rather than concentrated in a few names. The strategists believe that for the market to be stronger, the rest of the 493 companies in the index need to participate in the gains. While some believe a cyclical trade will eventually lead the market higher, there is disagreement about when this will happen.

The S&P 500's recent losses could be healthy for the overall index as it relies heavily on the performance of the "Magnificent Seven" stocks. Wall Street strategists believe that a convergence of gains across a broader range of companies, known as market breadth, would indicate a healthier stock market. While the outperformance of the Magnificent Seven is not abnormal, some experts argue that a shift in leadership is underway and that the other 493 stocks in the S&P 500 will eventually lead the market higher. However, there is disagreement about when this shift will occur, with some expecting a cyclical trade to take over soon, while others believe further valuation declines are needed before new leadership emerges.

The stock-market rally has broadened beyond the dominant tech giants, with a wider range of stocks participating in the S&P 500's upswing. This expansion in market breadth is seen as a positive sign for the sustainability of the bull market. Sectors such as industrials, financials, materials, energy, and real estate have seen increased investment, while the tech-heavy sectors have also performed well. The market's advance is supported by hopes of a soft landing for the U.S. economy, receding inflation pressures, and expectations for the end of the Federal Reserve's monetary tightening campaign. However, some analysts warn that the broadening rally and bullish sentiment may lead to overbought conditions and a potential correction in the future.

Despite reaching overbought levels, the stock market still has room to run as confirmed sell signals have not been registered yet. Major resistance is at 4650, and a pullback to support at 4440 would close gaps on the chart. Market breadth indicators, such as breadth oscillators and cumulative volume breadth, remain bullish. Volatility derivatives and VIX buy signals also support a bullish stance. Recommendations include potential CVB buy signal and a put-call ratio sell signal in Edwards Lifesciences. Trailing stops and rolling procedures are being used for existing positions.

The stock market rally showed strong, broad gains, especially late in the week, with market leadership remaining narrow, concentrated in the artificial intelligence space, as well as chips and software. Tesla broke out Friday, while DexCom, Lennar, and JPMorgan Chase flashed early entries late in the week. Apple is expected to show off its mixed-reality headset on Monday, its first new hardware product since the Apple Watch in 2015. Investors should be looking to add exposure amid the promising bullish shift, but be ready to step back.

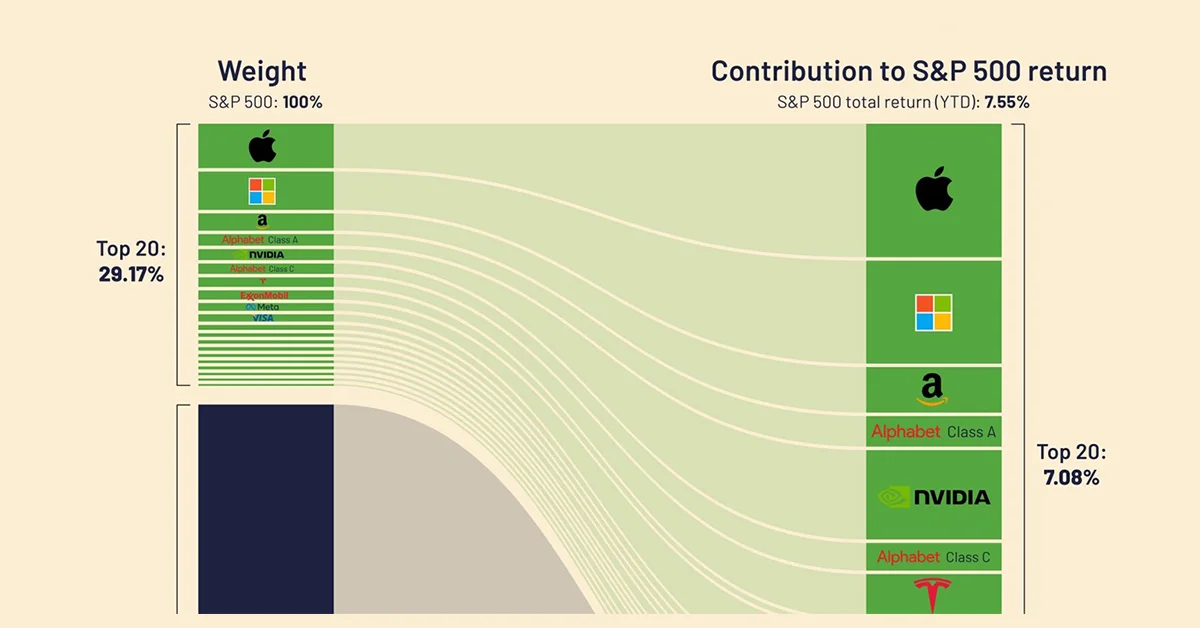

Just 20 companies, mainly AI-related stocks, are driving the S&P 500 into positive territory, with tech and AI stocks soaring amid market headwinds. The narrow market breadth signals growing risk in the market, as a small collection of companies make up over 29% of the entire index's market capitalization. Without the AI-led rally, the S&P 500 would be returning -1.4%.