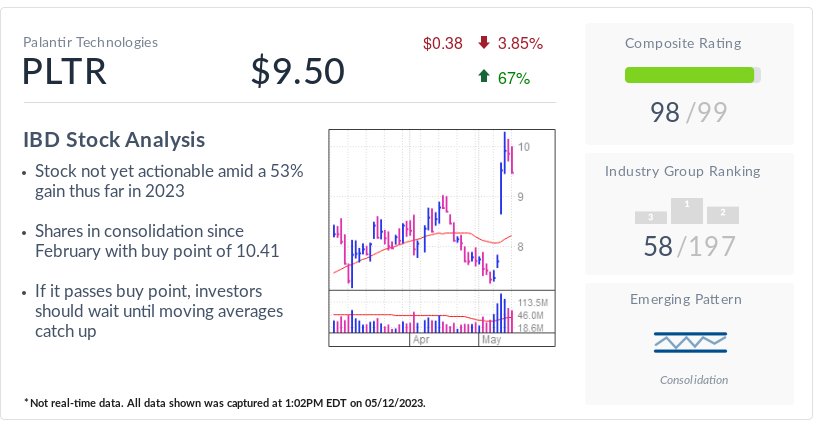

Palantir’s Growth Engine Justifies a Premium Valuation

Palantir’s Q1 results show accelerating growth powered by its AI Platform, with revenue up 85% YoY to $1.63B—the 11th straight quarter of accelerating growth—driven by strong US commercial demand and a government win (USDA). Margins are robust (adjusted operating margin 60%, GAAP net income margin 53%), and the company posts a Rule of 40 of 145% with net revenue retention at 150%, signaling a durable moat. Valuation remains premium (forward P/S ~42x, forward P/E ~93x), but analysts see potential upside if EPS doubles and growth persists; Palantir sits on a debt-free balance sheet with roughly $8B in cash. Overall, while expensive, the growth trajectory and margins make a compelling case for a long-term buy for some investors, with a Moderate Buy consensus and about 45% upside to a ~$188 target.