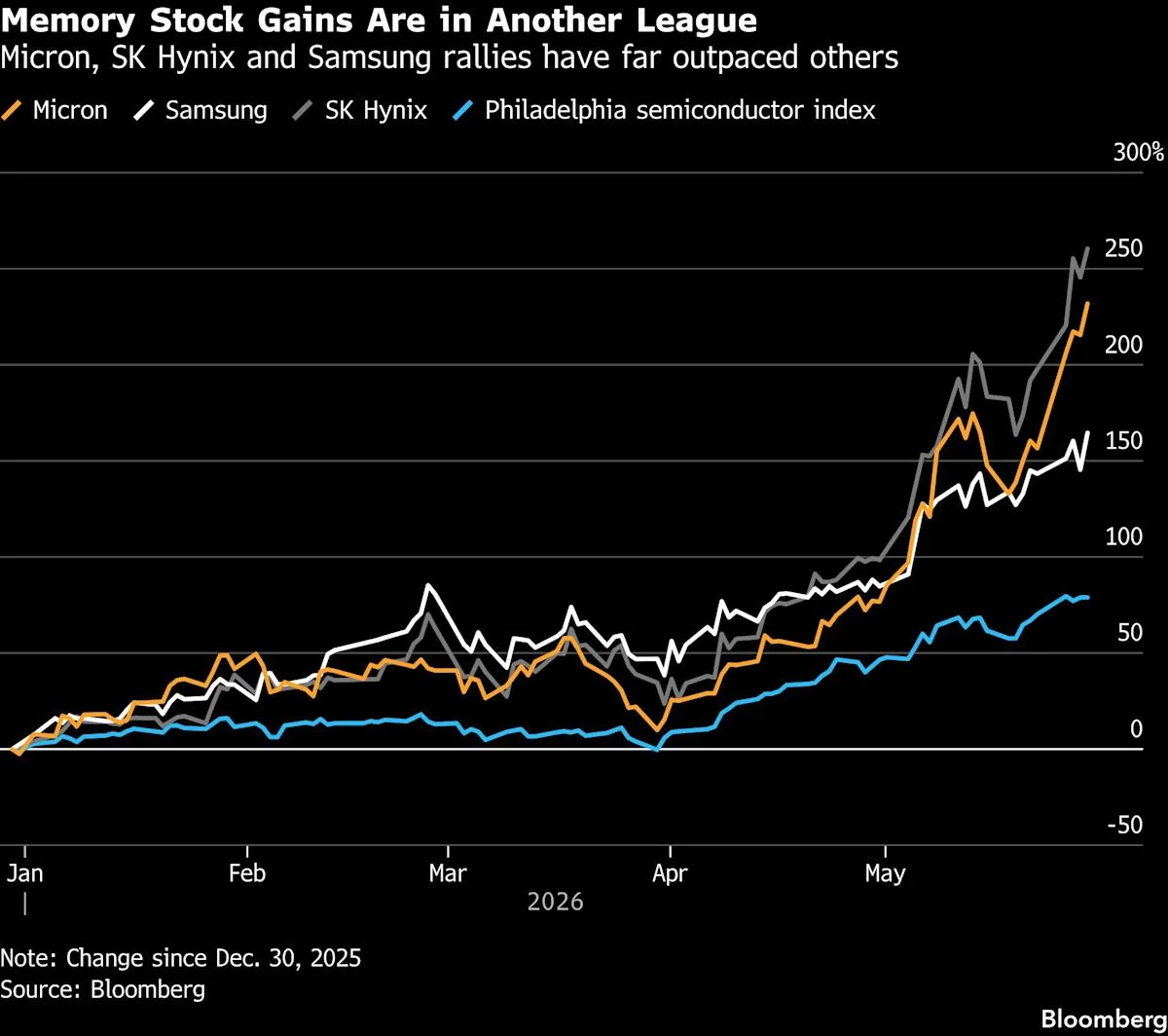

Semiconductor equities fell after Samsung beat profits but missed lofty AI demand expectations, dragging memory names and leading chipmakers lower as investors reassess whether AI spending can sustain the recent price run-up.

US stocks rose on the last trading day of the second quarter of 2026, with the Dow nudging to a fresh record above 52,000, the S&P 500 up 0.8% for its best quarter since 2020, and the Nasdaq up about 1.5% as chip stocks led the rally; the Philadelphia SOX posted its best quarter on record. Investors weighed a stronger dollar and yen weakness against signs of Fed independence after a Supreme Court ruling and potential US-Iran talks, while oil slid and markets awaited the June jobs report.

U.S. stocks rose Tuesday with the Dow up about 0.1%, the S&P 500 up 0.3%, and the Nasdaq up 0.8% as chip shares led gains into the quarter’s end. Investors weighed a stronger dollar and falling oil against a backdrop of a Supreme Court ruling that preserves Fed independence and expectations for the June jobs report, while eyeing potential US-Iran talks in Qatar and Nike’s upcoming earnings.

Micron posted a blowout quarter with revenue up about 346% and EPS up more than 10x, alongside gross margins near 85% and operating margins around 80%. The memory shortage is expected to persist through 2028, lifting memory prices and benefiting peers across the chip field. Management highlighted edge AI as a major growth driver, projecting increased memory demand in PCs and smartphones as AI expands beyond data centers. If edge AI accelerates, Intel, AMD, Arm, and Qualcomm could see a boost as AI-enabled devices become more prevalent in smartphones, PCs, and other gear.

US stocks fluctuated Friday after a New York Times report suggested OpenAI might delay its mega-IPO, weighing on memory-chip names even as the Nasdaq rose about 0.2% and the S&P 500 and Dow posted small gains; investors also weighed persistent memory-cost pressures on device makers, a strong Micron earnings signal of ongoing squeeze, potential Fed rate moves, and oil’s decline amid Middle East tensions.

US stocks were volatile on Friday as a New York Times report that OpenAI may delay its mega-IPO weighed on tech shares, leaving the Nasdaq near flat while the Dow and S&P 500 edged higher around 0.1%. Memory-chip cost pressures and Apple's price hikes signaled ongoing device-maker headwinds, with Micron’s earnings hinting the squeeze could persist. The OpenAI delay chatter, coupled with stronger May PCE inflation data, kept rate-hike bets alive, while oil slid about 3% amid Strait of Hormuz tensions.

Overnight trading showed Nvidia, Micron, Intel and AMD rising on news of a formal Iran peace deal, with MU and AMD leading gains around 7–9%, INTC up about 5–6%, and Nvidia up roughly 2%; broader semiconductor and memory ETFs also climbed as global markets advanced ahead of a Federal Reserve meeting.

U.S. stock futures climbed Monday as chipmakers steadied after Friday’s rout, led by gains in Nvidia, Broadcom and Micron; investors weigh AI-driven growth against renewed Middle East tensions and higher oil prices, with Citi lifting its 2026 S&P 500 target and Marvell set to join the index.

Asian equities fell as tech and chipmakers pulled back after Broadcom’s mixed results; U.S. stock futures slipped and risk appetite remained cautious amid unresolved U.S.–Iran tensions, with Japan’s Nikkei leading declines as BOJ officials signaled caution on rate hikes amid inflation risks; other regional indexes also traded lower.

The AI hype-versus-reality debate heats up as a broad rally in chip and tech stocks—led by Nvidia and peers like Microsoft—pushes markets to historic highs and reshapes investor expectations about the AI boom’s sustainability.

Chip stocks slipped after the U.S.-China summit ended without major technology deals, signaling cautious investor sentiment toward the sector even as a handful of tech names showed mixed moves during the session; broader semiconductor-related instruments traded lower in a risk-off atmosphere as markets digested limited progress and potential policy implications.

AI chip stocks including INTC, NVDA, and AMD rose in premarket trading on May 13, 2026, as investors grew more optimistic about AI demand and global trade sentiment, boosted by expectations that President Trump’s visit could help semiconductor sales in China. Nvidia, Intel, and AMD rose roughly 2% or more, QCOM around 4%, with MU and SNDK also higher. The rally reflects expectations of stronger data-center and cloud spending on AI, but risks remain from elevated valuations and potential geopolitical tensions; UBS remains bullish on the long-term AI investment trend.

Micron (MU) erased roughly $100 billion in market value at Tuesday’s low, but buyers quickly stepped in, turning what looked like a major breakdown into a test of demand near the $700 area and helping lift peers in the chip sector as memory supply tightens and AI-memory bets stay in focus. The rebound spread through the semiconductor group, with names like NVDA, AVGO, TXN, ADI, ON, and STX rallying as traders weigh whether MU can hold the key $700 level. Analysts remain bullish, with a Strong Buy consensus and an average price target around $608.33 per share.

Chip stocks that led the rally are showing weakness as traders rotate out of winners: notable decliners include Teradyne (~5.4%), Applied Materials (~5.9%), and NXPI (~2.7%), while other indices and tech names posted mixed moves (Spotify down about 12%, Enphase ~2.7% lower, etc.). The snapshot signals a cooling of the recent chip-led run and renewed market volatility as investors reprice risk across equities.