Semiconductor equities fell after Samsung beat profits but missed lofty AI demand expectations, dragging memory names and leading chipmakers lower as investors reassess whether AI spending can sustain the recent price run-up.

Hon Hai Precision Industry (Foxconn) reported a about-40% jump in June-quarter revenue to NT$2.51 trillion, beating forecasts around NT$2.37 trillion as AI-related server assembly with Nvidia accelerators drives demand. The company cautioned about memory-chip shortages but remains well-positioned thanks to AI infrastructure spending by major tech players and its role in Apple device assembly.

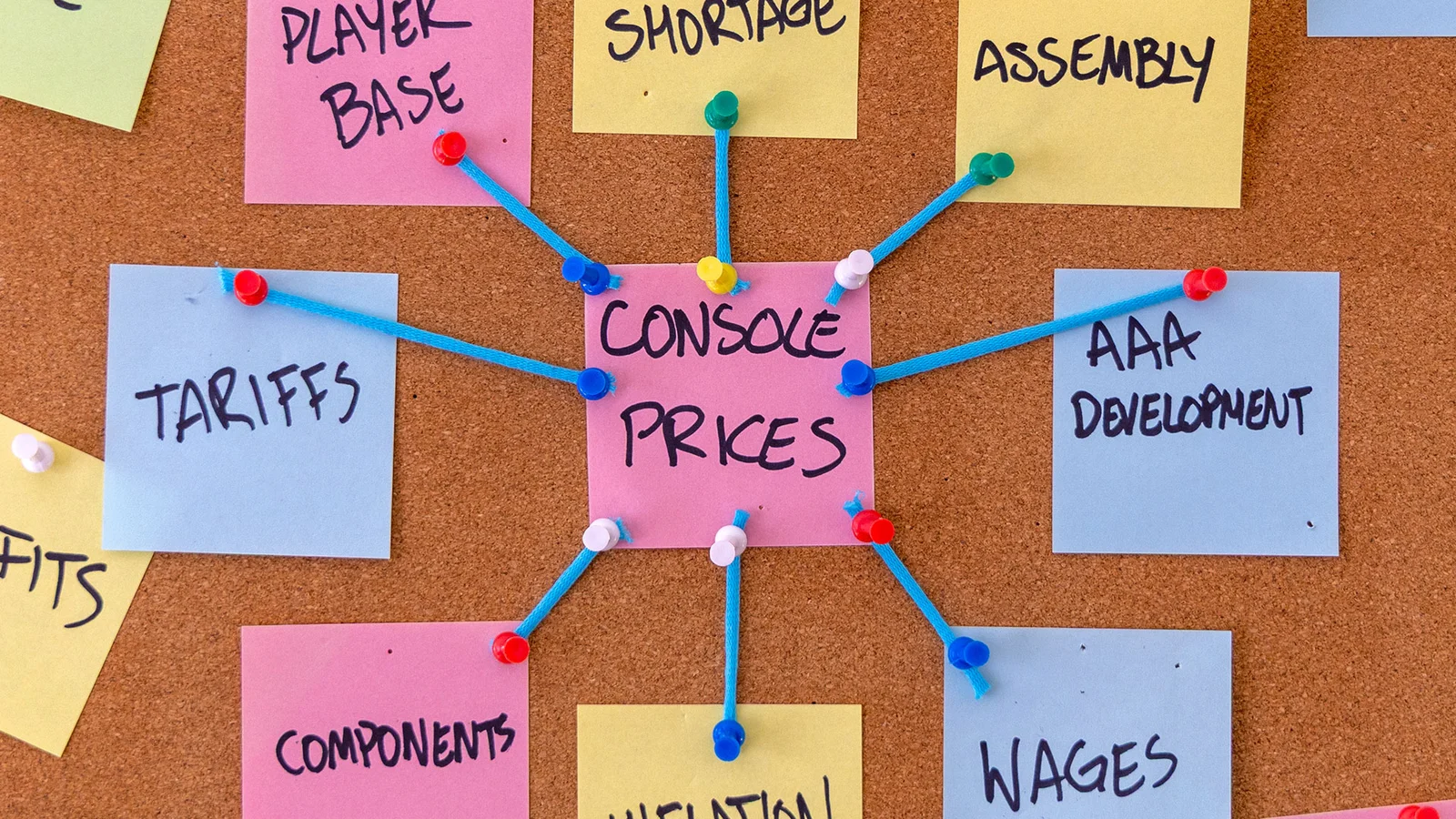

Microsoft raises Xbox Series S price to $499.99 by Aug 1, 2026, and PS5 Pro has climbed about $200 since its 2024 debut, as AI-driven memory demand and data-center expansion tighten supply. With gamers increasingly opting for handhelds and mobile gaming, plus higher development costs and inflation, the console market faces pricier hardware and a shrinking audience—potentially lasting into the 2030s.

Micron Technology posted a blowout fiscal Q3 2026 as DRAM and NAND demand far outpace supply, with revenue up 346% year over year and EPS surging more than 1,200%. Management projects capex of about $27 billion for fiscal 2026, likely rising above $40 billion in fiscal 2027, as AI workloads keep memory demand strong into the next decade. This tight memory market also supports Lam Research, a key memory-fab equipment supplier, contributing to an upbeat outlook for AI infrastructure stocks.

Chip stocks rode a record-breaking quarter driven by AI hardware demand, with the Philadelphia Semiconductor Index surging as memory and AI-related names led gains. But last week’s pullback and ongoing intraday swings underscore a more volatile path ahead, as investors weigh whether hyperscalers’ continued AI spending, stretched valuations, and memory bottlenecks can sustain the rally through the rest of 2026.

Analysts say RAM and other component costs will keep Apple prices rising through the next few years, with any relief unlikely before 2028 when new capacity comes online. Ongoing AI and compute demand may absorb gains, limiting potential price drops; if you're buying soon, consider acting sooner or purchasing through third-party retailers to secure lower prices.

Industry forecasts indicate RAM prices will stay elevated through 2028 due to AI-driven demand and supply constraints, with analysts warning of continued price hikes for PCs and consoles and potential delays for next-gen hardware like PlayStation 6.

Jefferies Equity Research warns memory prices for DRAM/NAND are set to rise through 2026 due to persistent shortages and limited new capacity, forecasting a 40–50% price jump in Q3 2026 and a further 30–40% in Q4, with 2027 YoY increases of 40–45% and only modest relief by 2028 as 15–20% more supply comes online. Long-term contracts with hyperscalers are tightening near-term supply, and Chinese memory firms are not expected to disrupt markets in 2026–27, though expansions could shift the landscape by 2028.

Micron posted a blowout quarter with revenue up about 346% and EPS up more than 10x, alongside gross margins near 85% and operating margins around 80%. The memory shortage is expected to persist through 2028, lifting memory prices and benefiting peers across the chip field. Management highlighted edge AI as a major growth driver, projecting increased memory demand in PCs and smartphones as AI expands beyond data centers. If edge AI accelerates, Intel, AMD, Arm, and Qualcomm could see a boost as AI-enabled devices become more prevalent in smartphones, PCs, and other gear.

Rising memory-chip costs driven by AI data-center demand are expected to push RAM prices higher and slow PC and smartphone shipments in 2026, with Apple already raising prices for Macs and iPads and retailers like Best Buy signaling potential margin pressure as suppliers pass along higher costs; Gartner projects PC prices up about 17% and smartphone prices up about 13%, while shipments could fall roughly 10% for PCs and 8% for smartphones, though the consumer impact may be gradual.

Apple announced price increases for its MacBook and iPad lines as memory and storage costs rise due to surging demand from AI data centers, detailing specific jumps (MacBook Neo $599→$699, MacBook Air 512GB $1099→$1299, MacBook Pro 1TB $1699→$1999, iPad Air 128GB $599→$749, iPad Pro Wi‑Fi 256GB $999→$1199) and signaling more hikes to come.

US stock futures steadied after a tech rout, with Nasdaq-100 futures up about 0.6% and S&P 500 futures up around 0.2% as investors await Micron’s earnings for a read on AI demand; the open comes after tough sessions for AI-related names, while traders weigh valuations and potential rate hikes as the market braces for a possible rebound.

Micron Technology (MU) slid over 10% in Tuesday trading ahead of its Q3 results, even as Bank of America hiked its price target by 58% to $1,500, citing a larger semiconductor total addressable market (about $2.7 trillion by 2030) and stronger AI, cloud, and data‑center demand for memory and chips; MU’s strategic partnership with Anthropic and improving automotive/industrial markets underpin the more bullish outlook despite the near‑term pullback.

Apple CEO Tim Cook says rising memory and storage costs make price increases unavoidable for Apple devices, with no specifics on which products or by how much. The Wall Street Journal notes AI-driven demand and chip shortages are driving costs, and analysts suggest prices could rise notably to maintain margins. Apple has already bumped the Mac mini from $599 to $799 and has trimmed some higher-tier Mac mini/Mac Studio options. Cook says Apple will use cash to boost memory supply but won’t build its own memory factories. Expect higher prices across iPhones, iPads, and Macs in the near term.

Micron Technology (MU) heads into its fiscal third-quarter earnings on June 24 with AI-driven memory demand helping revenue and a strong year-to-date gain, but analysts see meaningful downside: the average price target from 39 analysts is about $684.26 (high $1,750, low $125), implying roughly 28–30% downside from the current around $971. GuruFocus’ GF Value also suggests ~28%–30% downside to about $694, despite solid AI-related demand and revenue growth. The piece therefore leans toward MU being a sell/trim idea before the earnings print.