China’s EV push fuels 80% June rise in passenger-car exports as domestic demand weakens

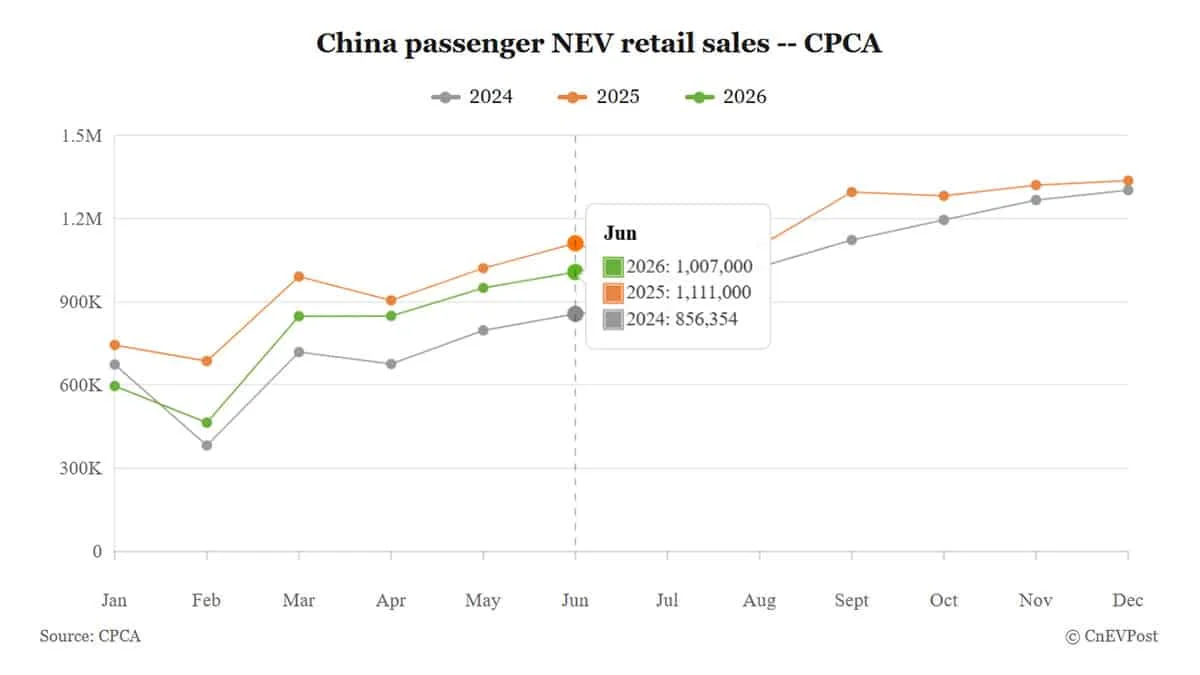

China’s passenger-car exports surged 80% year-on-year in June, driven by strong demand for electric vehicles, while domestic sales declined about 26%. For the first half of 2026, exports jumped 72% to over 4.4 million vehicles, with June exports around 905,000 cars (up from 809,000 in May). Analysts say the domestic market remains under pressure from price wars and a sluggish property sector, compounded by cutbacks in EV subsidies; meanwhile Chinese automakers like BYD are expanding overseas. Some forecasts suggest 2026 exports could reach around 10 million vehicles, though domestic demand may stay soft.