The article reports that former President Donald Trump praised rising inflation, saying “I love the inflation,” while alleging the U.S. is covertly seizing Iranian oil as part of energy and foreign-policy efforts, in the context of a 4.2% CPI rise and related commentary on energy prices.

CNBC host Jim Cramer calls the elevated CPI readings 'artificial inflation' and outlines what the development could mean for stock prices and market expectations.

US CPI data show airfare up 30% in five months (26.7% year over year), driven by higher jet-fuel costs linked to the Iran conflict and seasonal demand. Airlines have been raising fares to offset fuel costs, and with much of the industry signaling fares will stay elevated even if oil prices ease, the premium travel segment is driving most of the increase.

President Donald Trump reacted to the latest CPI data by saying 'I love the inflation' after the consumer price index rose to 4.2% year over year—a three-year high—with core inflation at 2.9%. He framed the rise as positive and tied it, in part, to U.S. actions against Iran, claiming credit for oil disruptions, though the link to prices was unclear. Economists forecast core inflation around 2.9%, and White House inquiries for comment were noted.

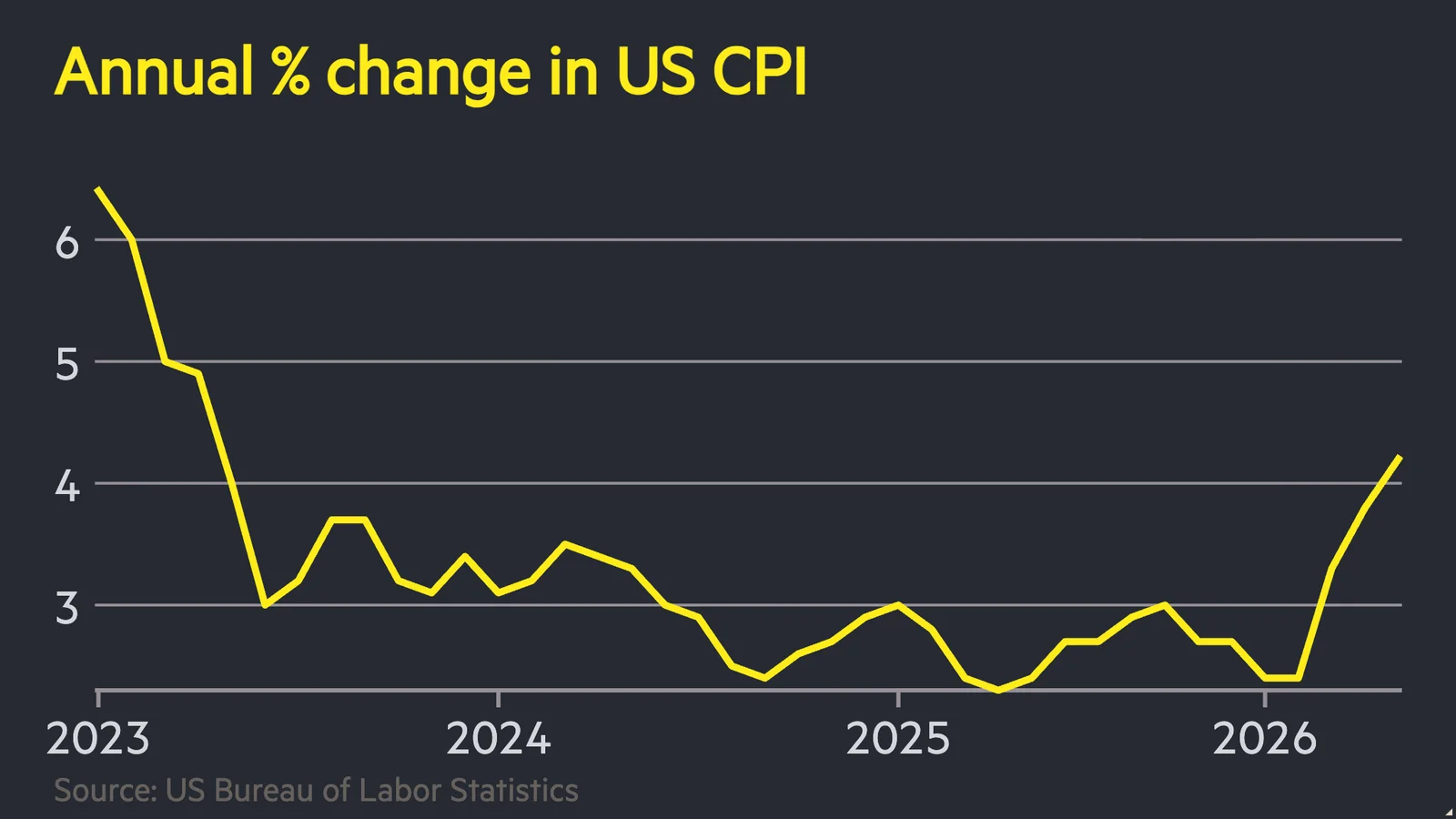

The May CPI rose 0.5% month-over-month and 4.2% year-over-year, the strongest annual reading in three years, driven mainly by a 3.9% jump in energy costs. Core CPI advanced 0.2% for the month and 2.9% over the year. Food costs rose 0.2% and shelter 0.3%, while transportation services fell 0.6% and used vehicles edged up. With inflation showing energy-driven pressure but some cooling in core measures, markets expect the Fed to hold rates at the June meeting as traders monitor energy prices and broader price signals.

Inflation likely rose for the third straight month in May as the Iran conflict boosted energy costs; economists expect the CPI to show about 4.2% year-over-year inflation with core inflation near 3%, keeping Fed rate hike bets on the table while tariffs and supply constraints could sustain price pressures.

Economists expect the May Consumer Price Index to rise about 4.2% year over year—the fastest since April 2023—with core inflation near 2.9%. Higher energy and fuel costs are the main drivers, though some energy prices have since eased. Inflation remains above the Fed's 2% target and is shaping household budgets, with a CBS poll noting about three-quarters of Americans feel incomes aren’t keeping up.

U.S. stock futures slipped after U.S. launched self-defense strikes against Iran, with S&P 500 and Nasdaq futures down about 0.3% and Dow futures off around 161 points; oil rose about 1% to near $89 as tensions escalated. In regular trading, the Dow edged up about 0.17% while chip stocks dragged, and investors await May CPI data due Wednesday (consensus 4.2% y/y, 0.5% m/m), a signpost for inflation amid ongoing geopolitical risk and AI-led market moves.

The May consumer price index is due Wednesday at 8:30 a.m. ET, with consensus calling for a 4.2% annual inflation rate and a 0.5% monthly gain, the first CPI above 4% since May 2023. Core inflation is expected to be 2.9% year over year and 0.3% monthly. The report signals broader inflation pressures as energy prices rise and supply disruptions persist, with implications for markets and policy.

With the May CPI data due after a stronger-than-expected jobs report sparked a market sell-off, analysts expect headline CPI to rise about 0.5% month-over-month (4.2% year-over-year) and core CPI to 0.3% (2.9% YoY). Markets are pricing in higher policy rates, with December 2026 rate-hike odds around 65%. The May CPI release, together with the Fed’s policy statement and projections, could be a pivotal inflection point for monetary policy and risk assets amid persistent inflation and solid hiring.

SpotGamma warns that June’s catalyst-packed calendar could trigger a volatility spasm and test the nine-week stock rally: May CPI data due June 10 amid energy-cost pressures, SpaceX’s June 12 IPO with potential Russell index inclusion, and a busy mid-June schedule capped by a Fed decision and quadruple witching options expiry. The note points to stretched bullish positioning in AI names and hedging in IWM puts and SPY protection, plus notable XSP put-diagonal activity as traders seek downside protection. If upside demand eases and calls unwind, a sharper pullback could follow even as the market sits near record highs.

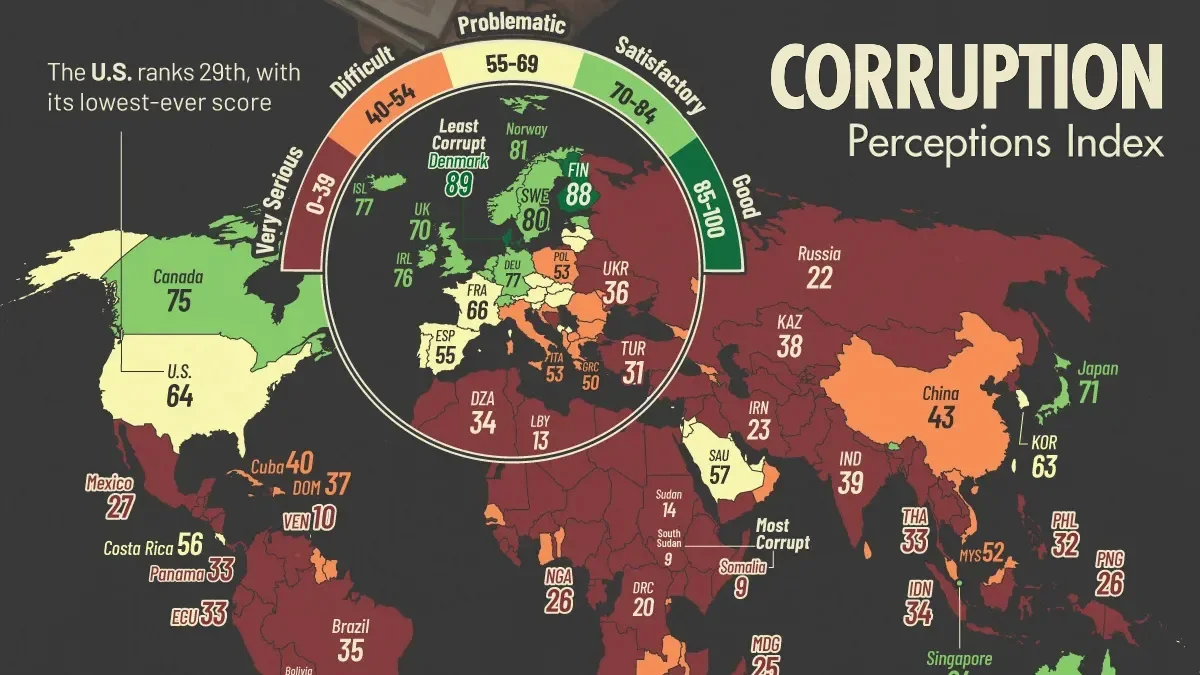

Global corruption perceptions fell to 42/100 in 2025, shrinking the number of top-scoring countries to just five (Denmark, Finland, Singapore, New Zealand, Norway) and leaving the United States at 64 in 29th place, its lowest CPI result on record. The piece ties the decline to rising polarization and weaker institutional checks. Separately, Freedom House’s 2026 rankings crown Finland at 100 and put the United States at 81, with Europe leading and the least-free nations clustered in Africa and Asia (e.g., South Sudan, Sudan, Turkmenistan, North Korea). The article also notes the human costs of corruption—including threats to journalists—and the importance of independent media and strong institutions in combatting graft.

A hotter-than-expected CPI reading suggests inflation may prove stickier than hoped, prompting the Fed to stay cautious and lifting odds of further rate hikes; markets price in a longer, higher-for-longer path for policy as investors reassess timing of monetary tightening.

US consumer prices rose 3.8% year over year in April, the fastest since 2023, driven by surging energy costs tied to the Iran conflict; gas averages about $4.50 a gallon, with housing and groceries also lifting inflation, keeping Federal Reserve rate cuts unlikely this year.